Income may arrive with great fanfare and depart with equal speed. Wealth, by contrast, tends to grow quietly, almost invisibly.

By: Raphic Burdo

Among the many misconceptions that shape modern economic life, none is more pervasive than the confusion surrounding wealth.

We speak of it constantly. We pursue it, admire it, envy it, tax it, inherit it, lose it, and occasionally write books about it. Yet for all the attention devoted to wealth, I am of the view that many otherwise intelligent people misunderstand its most fundamental characteristic. They mistake income for wealth and wealth for income.

At first glance, the confusion seems harmless. After all, money is money. If one person earns more than another, it seems reasonable to assume that the higher earner will eventually become wealthier. Indeed, much of modern life is organized around this assumption. Students are encouraged to seek high-paying professions. Universities advertise the salaries of their graduates. Parents proudly tell relatives what their children earn. Newspapers publish annual lists of the highest-paid executives, athletes, entertainers, and entrepreneurs. The implicit message is unmistakable: earn more and you will become wealthy. Yet, in fact, the matter is not quite so straightforward.

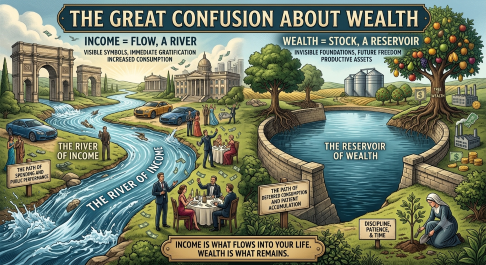

Over the years, I have encountered individuals, you may also have met a few, who earned extraordinary incomes and nevertheless remained financially insecure. On the other end of spectrum, I have also met schoolteachers, engineers, civil servants, small shopkeepers, and farmers who never enjoyed spectacular earnings but gradually accumulated substantial wealth. The first group often appeared prosperous; the second frequently appeared ordinary. Yet appearances, as they so often do, concealed more than they revealed. This observation raises an uncomfortable yet important question: if wealth is simply the result of income, how can such contrasting outcomes occur. The answer to this, in my opinion, is that income and wealth belong to different categories of economic reality. Income is what flows into your life. Wealth is what remains. This distinction appears simple, but entire lives are shaped by whether one understands it.

Read: What is the difference between income and wealth?

Economists sometimes describe income as a flow and wealth as a stock. Although the terminology may sound technical, the underlying idea is remarkably intuitive. Consider a river and a reservoir. The river represents income. Water is constantly flowing through it. The reservoir represents wealth. Water accumulates there over time and remains available long after the rain has stopped. A person may enjoy a mighty river of income and yet possess a very small reservoir. Another may have only a modest stream of income but a surprisingly large reservoir. The size of the river certainly matters. However, what ultimately determines long-term security is not merely how much water passes through the system, but how much is retained.

I sometimes suspect that our fascination with income stems from the fact that income is visible. Salaries can be announced. Promotions can be celebrated. Bonuses can be discussed at dinner parties. Wealth, by contrast, is often invisible. No one notices the shares quietly accumulating in an investment account. Few people admire a declining mortgage balance. The patient acquisition of productive assets rarely attracts attention. Human beings are naturally drawn toward visible symbols of success. Consequently, societies often celebrate the appearance of wealth while overlooking its foundations. This confusion has become particularly pronounced in the modern age.

Consumer culture, aided by advertising, social media, and easy credit, has transformed spending into a public performance. Never before have had individuals possessed so many opportunities to display prosperity. Cars, watches, homes, holidays, clothing, restaurants, and electronic devices have become symbols through which people communicate status. Yet there is an irony here. Many of the things commonly associated with wealth are not signs of wealth at all. They are signs of expenditure. A luxury car may indicate wealth. But it may also indicate debt.

A large house may reflect financial strength. It may equally reflect financial strain. Expensive possessions reveal remarkably little about the condition of a person’s balance sheet. Indeed, one of the paradoxes of economic life is that wealth is often least visible among those who possess the most of it. This observation is not new. Throughout history, thoughtful observers have noticed that genuine wealth tends to accumulate quietly. The merchant families of Renaissance Italy, the trading communities of South Asia, the industrial entrepreneurs of nineteenth-century Britain, and countless family businesses around the world all understood a principle that remains true today: wealth grows through ownership, patience, and accumulation rather than through display. The world notices the mansion. It rarely notices the decades of disciplined decisions that made the mansion possible.

Moreover, there is a psychological dimension to this discussion that deserves attention. I am persuaded that the greatest obstacle to wealth is often not low income but an inability to define what constitutes enough.

Human desires possess an extraordinary capacity for expansion. When income rises, expectations tend to rise alongside it. What once appeared luxurious soon becomes normal. What once seemed unnecessary gradually becomes essential. A larger home, a better car, more exclusive experiences, and increasingly expensive habits are absorbed into everyday life. This process occurs so gradually that many people fail to notice it. They earn more each year and yet feel no closer to financial freedom. Their standard of living improves, but their financial security remains elusive. The problem is not that they earn too little. The problem is that increased income is converted into increased consumption rather than increased wealth. This distinction may appear subtle, but its consequences compound across decades.

A young professional who saves and invests a modest portion of income year after year often accumulates more lasting wealth than a higher earner who spends nearly everything. This outcome strikes many people as unfair. Yet it is neither unfair nor mysterious. It is merely arithmetic operating over long periods of time. The ancient merchants who traded along the Silk Road understood this. So did Benjamin Franklin. So did the industrialists of the nineteenth century and many of the world’s most successful investors today.

While technologies, industries, and economic systems have evolved dramatically, the underlying mechanics of wealth have changed surprisingly little. First, value must be created. Secondly, a portion of that value must be preserved. Thirdly, preserved value must be transformed into productive assets. Finally, time must be allowed to perform its quiet work. The sequence sounds almost disappointingly simple. Yet simplicity should not be mistaken for ease. Every stage requires discipline. Every stage requires patience. Every stage also requires a willingness to sacrifice immediate gratification for future possibility.

This is why I am inclined to describe wealth as deferred consumption. Every meaningful asset represents something that could have been consumed but was not. A luxury postponed. An impulse resisted. A bonus invested rather than spent. A purchase delayed in favour of a more productive use of capital. Seen in this light, wealth becomes more than a financial phenomenon. It becomes a record of decisions made across time. It becomes evidence that an individual cared not only about present desires but also about future opportunities.

Indeed, the more we reflect upon the subject, the more convinced we become that wealth is fundamentally about freedom. Not because wealth guarantees happiness or eliminates suffering or solves every human problem but because wealth expands choice. It provides the freedom to leave an unhealthy workplace. The freedom to support one’s family during difficult periods. The freedom to pursue meaningful work rather than merely necessary work. The freedom to withstand adversity without panic. The freedom to think long-term when circumstances encourage short-term thinking.

Money itself possesses little intrinsic value. Its significance lies in the possibilities it creates. This, in my opinion, is the first great truth that every young person should understand. Do not confuse earning money with becoming wealthy. The two are related, but they are not identical. Income creates opportunity. Wealth emerges from what is done with that opportunity. The highest earners do not always become wealthy. The wealthiest individuals are not always the highest earners. The difference lies in understanding that money earned is only potential. Wealth arises when that potential is preserved, directed, and allowed to mature over time.

Over a long period of time, I am convinced that this distinction explains much of what we observe in economic life. Income may arrive with great fanfare and depart with equal speed. Wealth, by contrast, tends to grow quietly, almost invisibly. Like a tree, its progress is difficult to detect from day to day and remarkable when observed across decades. Perhaps that is why so many people misunderstand it. They notice the fruit. They rarely notice the years of growth that made the fruit possible.

Read: The Mules Mansion of Karachi

__________________

Raphic Burdo is a student of Literature, Psychology, Public Policy and Entrepreneurship. He writes on the subjects where all four intersect.